Mortgage rates for the week ending April 17, 2026 showed slight movement as markets digested the latest economic data and Federal Reserve commentary. Here is a breakdown of where rates stand this week, what is driving the changes, and what borrowers should consider as they navigate the spring housing market.

This Week’s Rates

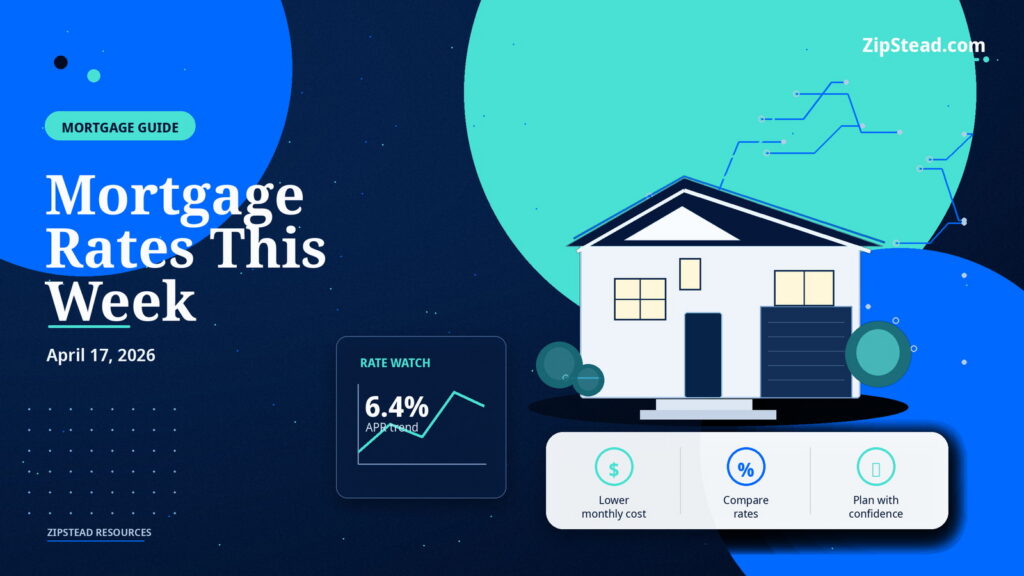

The 30-year fixed-rate mortgage averaged approximately 6.40 percent this week, holding relatively steady compared to the prior week. The 15-year fixed rate came in around 5.72 percent, also largely unchanged. Adjustable-rate mortgages (5/1 ARMs) continued to price in the mid-to-high 5 percent range, offering a modest discount over fixed-rate products for borrowers willing to accept rate adjustment risk after the initial fixed period.

Jumbo loan rates — for loan amounts exceeding $766,550 in most markets — averaged roughly 6.55 to 6.70 percent, maintaining the typical premium over conforming loan rates.

For context, these rates remain well above the historic lows of 2020 and 2021, when 30-year fixed rates briefly dipped below 3 percent. However, they are within the range that economists have forecasted for most of 2026, and they remain below the 7-plus percent peaks that borrowers faced in late 2023.

What Is Driving Rates This Week

Several economic factors influenced rate movement during the week of April 17.

The 10-year Treasury yield, which serves as the primary benchmark for mortgage rate pricing, traded in a narrow band through most of the week. Treasury yields have been held in check by a combination of moderating inflation data and cautious consumer spending numbers, which signal that the economy is cooling slightly without tipping into recession.

The Federal Reserve continued to signal patience on rate cuts. While the Fed has lowered the federal funds rate modestly from its 2023 peak, officials have made clear that further cuts will depend on sustained progress toward the 2 percent inflation target. The consumer price index for March came in slightly above expectations, which tempered hopes for a near-term rate cut and kept mortgage rates from falling further.

Labor market data released earlier in the month showed continued job growth but at a slower pace than 2025, with wage growth moderating. This mixed picture — a still-healthy but cooling economy — has kept mortgage rates in a holding pattern rather than moving decisively in either direction.

Rate Trends Year to Date

Looking at the broader trajectory, mortgage rates have fluctuated within a relatively narrow range during the first four months of 2026. The 30-year fixed rate started the year around 6.5 percent, dipped briefly toward 6.2 percent in February on optimistic inflation data, then drifted back up toward 6.4 percent as subsequent economic reports came in mixed.

This sideways pattern reflects the market uncertainty about the pace of future Fed rate cuts. Investors are pricing in one to two additional cuts by year-end, but the timing remains unclear. Until there is a decisive signal — either a meaningful drop in inflation or a more significant economic slowdown — mortgage rates are likely to continue trading in this 6.2 to 6.6 percent range.

What This Means for Homebuyers

If you are in the market to buy a home this spring, here is how to think about the current rate environment.

Do not wait for a dramatic rate drop. The consensus among major forecasters — including Fannie Mae, the Mortgage Bankers Association, and the National Association of Realtors — is that rates will remain in the low-to-mid 6 percent range through the second half of 2026. Hoping for a return to 5 percent or lower is not a realistic strategy for the foreseeable future.

Focus on what you can control. Your credit score, down payment amount, debt-to-income ratio, and loan type all influence the rate you personally receive. A borrower with a 780 credit score and 20 percent down will typically qualify for a rate 0.25 to 0.50 percent lower than a borrower with a 680 score and 5 percent down. On a $350,000 loan, that difference translates to roughly $50 to $100 per month in savings.

Shop multiple lenders. Rate quotes can vary by 0.25 percent or more between lenders on the same day for the same borrower profile. Getting quotes from at least three lenders — including a bank, a credit union, and an online lender — can save you thousands over the life of the loan. Comparison shopping within a 14-day window counts as a single credit inquiry, so there is no downside to getting multiple quotes.

Consider points strategically. Paying discount points (each point equals 1 percent of the loan amount) to buy down your rate can make sense if you plan to stay in the home long enough to recoup the upfront cost. At current rates, buying one point typically lowers your rate by 0.20 to 0.25 percent and breaks even in roughly four to five years. If you expect to stay longer than that, points can be a smart investment.

What This Means for Sellers

Sellers benefit when mortgage rates are stable because stability reduces buyer uncertainty. In a volatile rate environment, buyers hesitate — they worry about locking in at the wrong time or getting priced out by a sudden spike. The steady rate range we have seen in early 2026 has helped maintain buyer confidence, even if the overall pool of qualified buyers is smaller than it was during the ultra-low-rate era.

If you are listing your home this spring, work with your agent to price strategically for the current rate environment. At 6.4 percent, a buyer purchasing a $400,000 home with 10 percent down faces a monthly principal and interest payment of approximately $2,250. Understanding your buyer affordability constraints helps you price your home at a level that attracts qualified offers without leaving money on the table.

Rate Lock Recommendations

For buyers who are under contract or close to making an offer, the current rate environment suggests a moderate approach to rate locks.

A 30 to 45-day lock is appropriate for most transactions. This gives you enough time to complete the loan process without paying a premium for an extended lock period. If your closing timeline is longer — say 60 to 90 days — the additional cost of an extended lock (typically 0.125 to 0.25 percent) is usually worth the protection against a potential rate increase.

Float-down options are available from some lenders and allow you to lock your rate now but adjust downward if rates drop before closing. These options typically come with a small fee but can provide peace of mind in an uncertain rate environment.

Looking Ahead

The next major data points that could move mortgage rates include the April consumer price index release, the Federal Reserve next policy meeting, and the monthly jobs report. If inflation continues to moderate and the labor market cools further, there is a possibility that rates could drift toward the low end of the current range — closer to 6.2 percent — by late spring. Conversely, any inflation surprises or signs of re-accelerating economic growth could push rates back toward 6.5 percent or higher.

We will continue to track weekly rate movements and provide analysis on what they mean for buyers and sellers. For personalized rate guidance based on your specific financial situation and market, consult with a mortgage lender who can run scenarios tailored to your needs.

Rates referenced in this article are national averages and may vary based on your location, credit profile, loan type, and lender. Always obtain personalized rate quotes for the most accurate pricing.